How we charge

Not many financial advisers publish their fees on their websites. We do, because we believe in being transparent about how we charge for the work we do.

We also completely believe in the value we provide to our clients. In fact, research published by the International Longevity Centre UK (ILC) shows that those who receive professional financial advice boost their wealth by an average of £47,000*

Our clients have also told us how much they appreciate our advice and guidance – just take a look at their testimonials below.

We can offer a planning only service, without the requirement to take ongoing advice. However, we can provide the best value to those clients who choose to work with us over the long term.

* ILC Report: Peace of mind: Understanding the non-financial value of financial advice, written 16/11/2020.

Below are details of how we charge for each step of your journey with us:

1. Discover

The first step is to find out how your journey might look! We’ll discuss your financial objectives and goals, uncovering your priorities and timelines for achieving them. Where we are considering your investment needs, we’ll discuss your attitude and experience of investing, as well as the level of risk you can afford to take.

If you are interested in finding out whether your financial life plan is on track beyond retirement — and in answering the biggest question of all, ‘How much capital is enough?’ — then we can talk about our Truth About Money service, listed under our Additional Services menu.

Our charges

There is no charge for this step of your journey. All of the time we invest at the ‘discover’ stage is entirely at our expense.

2. Research & advice

With the information we have obtained from the ‘discover’ stage, we will create a plan which aims to achieve your financial goals, and investigate which products will be most suitable for your needs. At this point, we will agree on the initial and ongoing fees required to deliver your plan.

If you engage us for our separate Truth About Money service, we will work together to establish how close you are to funding the lifestyle you desire beyond retirement and, more importantly, what you can do to correct any shortfall.

Our charges

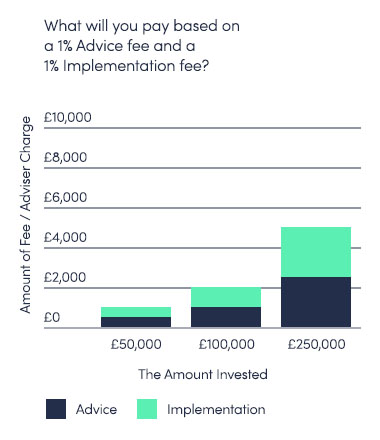

Investments and Pensions, Option 1: A percentage(%) of the amount invested.

Please note that these are maximums for each tier, which means actual charges will be case dependent and probably lower.

£0 -> £250,000: between 1.0% and 2.0%. Maximum charge £5,000

£250,001 -> £500,000: 0.75% Maximum charge £1,875

£500,001 -> £750,000: 0.50% Maximum charge £1,250

£750,001 -> £1,000,000: 0.25% Maximum charge £625

Over £1,000,000: 0.0%

The overall charge in this example would be £8,750 and assumes the maximum charge has been applied to each tier.

These fees can be paid to us by you directly, or can be deducted from your investment by the product provider.

Investments and Pensions, Option 2: Per hour.

We will provide you with a bespoke estimate of the time required before we commence any work and will not charge for any further work unless agreed with you. The charge is £250 per hour, (no VAT when we act as an intermediary between a client and a product provider).

The time taken to undertake the work will depend on the complexity of the advice. For instance, a single ISA recommendation will typically take 4 hours and an inheritance tax solution or multiple pension transfers involving several recommendations will typically take 20 hours.

Investments and Pensions, Option 3: Fixed charge.

We will confirm the fee amount once we have scoped the task and amount of work due. Mimimum £1,000.

Mortgages

There is usually no charge for this step of your journey. However, we do reserve to right to charge an initial fee at this stage for more difficult cases.

Equity Release Mortgages

There is usually no charge for this step of your journey. However, we do reserve to right to charge an initial fee at this stage for more difficult cases.

3. Implementation

We recommend and implement your strategy after explaining it to you. We will assist in the completion of any relevant paperwork, ensuring the documentation is processed as quickly and efficiently as possible.

Our charges

Investments and Pensions

There is no charge to you for this step of your journey. All of the time we invest at this stage is entirely at our expense.

Residential and Buy to Let Mortgages

There is usually no charge for this step of your journey, but we do charge a minimum of £1,000 when you receive your mortgage offer. Our minimum total earnings must be £1,500, some of which we will receive as commission from the mortgage lender. You will be notified of this when we provide you with the mortgage illustration, before a mortgage application is made.

Equity Release using Lifetime Mortgages

There is usually no charge for this step of your journey, but we do charge a minimum of £1,000 when you receive your mortgage offer. Our minimum total earnings must be £1,500, some of which we will receive from the mortgage lender. You will be notified of this when we provide you with the mortgage illustration, before a mortgage application is made.

The Three Hat Service

We charge £1,000 or £1,500 + VAT to produce your financial plan, depending on whether we are advising on other investments/pensions.

4. Ongoing service

We build long-lasting trusted business relationships with all of our clients. Whilst optional, we recommend that you continue to work with us to review your investment and pension planning on a regular basis, to ensure that they match your changing goals and objectives.

Our charges

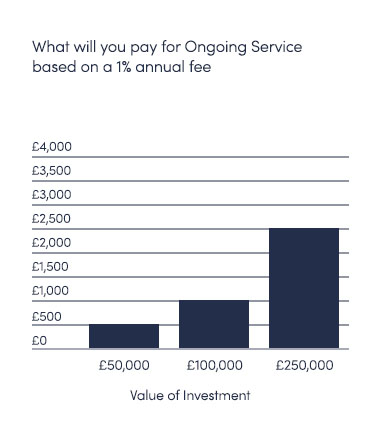

Investments and Pensions

We typically charge 1% of your total funds under management per annum for this service, (lower for investments exceeding £500,000). These fees can be deducted from your investment by the product provider, or paid to us by you directly.

This service includes:

- Regular meetings

- Your own client portal

- Annual report, including a discussion about your portfolio performance and ongoing appropriateness of the product(s)

- Fund switching, when necessary

- Top ups to certain products at no additional initial advice cost

- Bimonthly topical newsletter

- Easy access to your adviser throughout the year

- Unlimited questions

Mortgages

There is no ongoing fee paid to us.

Lifetime Mortgages

There is no ongoing fee paid to us.

Please note that we do not charge VAT for our services where we act as an intermediary between you and a product provider.

Fee Examples

If you would like to find out how we can help you to plan for today, tomorrow and the unexpected, why not get in touch?

Helping you plan for today, tomorrow and the unexpected

Receive our newsletter

Stewart said, in answer to these questions: 1. What could they have done better? “Nothing he was very good.” 2. What were the circumstances that caused you to initially look for an adviser? “I had pensions that I felt needed managing as I am not financially savvy.” 3. How has Mark Bastable helped you? “Managed my pensions and finally got me a good deal on an annuity.” 4. Have you seen the outcome you were hoping for? “Yes.”

Mark has provided me with financial advice for many years and recently has conducted a full pension review which led to moving funds to a new company resulting in a more modern and easy to access account that really suits my needs. Mark is very responsive, pro active and answers all questions in an easy to understand manner. Highly recommended!

Feedback from Steve to questions asked: What could they have done better? Nothing. What were the circumstances that caused you to initially look for an adviser? Pensions and ISA advice. How has Mark Bastable helped you? As above plus wider discussions around sensible financial planning and what expectations I should have form my current financial position. Have you seen the outcome you were hoping for? Yes. I am happy with the pension advice and ISA recommendations over the last 3 years.

I would highly recommend Mark Bastable of Templegate Financial Planning . He will give you solid advice that will definitely benefit your future finances. Everybody has different needs and plans , my ideas and my circumstances were certainly different from any other of his clients. However Marks strength is that he will listen very carefully then make suggestions that are more suitable to you personally. Giving a true tailor made service. His response time is remarkable, he always replied to my many, many questions instantly.

I met Mark a little over a year ago to hopefully take over my pension management from another Financial Advisor. I found Mark to be extremely thorough, pulling information out of me I didn’t realise I knew. The upshot is a Financial Advisor who has kept me on the straight and narrow, helping me to maintain value but meet my needs. A timely intervention recently when market values dipped helped to limit my fund being unnecessarily reduced allowing it to return value over recent months. Mark is on the ball and very helpful.

I highly recommend Mark Bastable. After a detailed Financial Review he patiently explained my Pension options as a couple of my pensions from previous employments were old and needed more further financial investigation. I found Mark to be professional, knowledgeable but also very personable and easy to communicate with. I am continuing to use his services for future investment advice.

We’ve had a great experience working with Mark. He has always given us clear, straightforward advice and taken the time to answer all of our questions, making sure we fully understand our options. He’s helped us save money by finding policies that genuinely match our needs, rather than a one-size-fits-all approach. He has improved our joint life insurance policy, improved our personal sick pay policies, and set up my pension as a stocks and shares ISA. He has also taken the time to discuss the importance of a will with us. We feel confident knowing our finances are well organised and in good hands.

I have been using Mark for his financial services for a few years, I like that he does all of the hard work to ensure the best outcome for my future financial security towards retiring and accommodates my very limited knowledge to achieve my goals. I would strongly recommend Mark for anyone looking for professional financial advice along with an approachable personality.

Mark took over my pension investments a few years ago and has been excellent. He has the ability to explain quite complicated options in a very clear manner whilst having the in depth knowledge to dive into the detail should you require it. Mark has a friendly manner and takes time to listen very carefully to your needs before fully explaining investment options. Mark is proactive and responds quickly to any question you may have at any time. It’s thanks to his advice my pension management costs have reduced and I have been pleased with the performance of the pension investment. I trust Marks advice, value his expertise, and I wouldn’t hesitate in recommending him to my family and friends.

Mark Bastable has recently provided a full review of our pensions and investments, taking time to understand our long-term goals and appetite for risk before making appropriate recommendations. He is very knowledgeable and responsive and answers any questions in easy-to-understand terms. We found the modelling of future income and costs based on different scenarios particularly useful and now have far more peace of mind that we are on track for the retirement we desire. We have no hesitation in recommending Mark.

I have been using mark for his financial services for a few years. I like that he does all the hard work to ensure the best outcome for my future financial security towards retiring and accommodates my very limited knowledge to achieve my goals. I would strongly recommend mark for anyone looking for professional financial advice along with an approachable personality.

My partner was taking early retirement and enlisted Mark's help. Unfortunately, he died unexpectedly leaving me with his estate and so I asked Mark for his help and advice. Without his help I would have not known where to start at this daunting time, but he has always given sound financial advice always with an empathetic, professional manner. I have been receiving financial advice from Mark for over 10 years. He is professional and very thorough focusing on my relevant financial matters as situations as things change from year to year. Initially I didn't have any expectations because I was still numb from bereavement but as the years have passed, I have been able to engage more and see the benefit from the investment plans Mark has made for me.